19

Mar

If you’re searching for adjusted r square formula pictures information related to the adjusted r square formula keyword, you have come to the ideal blog. Our site always provides you with suggestions for seeking the highest quality video and image content, please kindly hunt and find more informative video content and graphics that fit your interests.

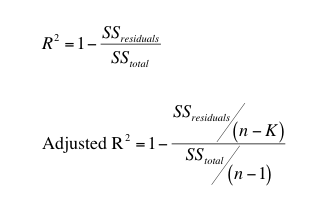

Adjusted R Square Formula. References Related Calculators Search. Adjusted R-Squared is Negative or Zero Adjusted R-Squared can be zero or negative in two conditions R² is very small or close to zero. Σ Y 2 square of Y score sum. This measures what proportion of the variation in the outcome Y can be explained by the covariatespredictors.

Adjusted R squared Formula The formula to calculate the adjusted R square of regression is represented as below R2 1 N Σ xi x Yi y σx σy2. While this identity works for OLS Linear Regression Models aka. Σ Y 2 square of Y score sum. Total Sum of Squares TSS Residual Sum of Squares RSS Explained Sum of Squares ESS. You should first run the fitmethod and save the returned object and then run the predictmethod on that object. Mathematically R-squared is calculated by dividing sum of squares of residuals SSres by total sum of squares SStot and then subtract it from 1.

R-square value and adjusted r-square value 0957 0955 respectively. Importantly its value increases only when the new term improves the model fit more than expected by chance alone. Well explain the concept of Deviance in a bit but for now lets look at this identity for nonlinear regression. While R² increases as variables are added the fraction n-1n-p-1 increases as variables are added. Results modelfit Running resultsparamswill produce this pandas Series. Adjusted R 2.

Previous post

Adjusted r squared formulaNext post

A stem and leaf plot